The Future of Health & Wellness

3 Bold Predictions About the Consumer Health & Wellness Industry in 2022 and Beyond

Last week, Fitt Insider Co-Founder and friend of mine, Anthony Vennare, posted a thought-provoking ask on LinkedIn — “Make a bold prediction about the health and fitness industry in 2022”.

This post got me thinking about the many founders and businesses I’ve had the pleasure of speaking with during my time as a Venture Associate at 14W and the hours of research I conducted on the evolving digital healthcare landscape. Through this extensive research, a handful of patterns began to emerge. Whether I was evaluating businesses in mental health, behavioral health, biohacking, dermatology, diabetes, health coaching, obesity, sleep, or otherwise, I noticed startups beginning to incorporate consumer best practices into their business models. This means combining outstanding customer experience, product simplification, and modern, millennial-friendly branding with more accessible, affordable, and personalized care.

Having recognized these shifts, I commented on Vennare’s LinkedIn post to briefly explain my predictions. Today, my intention is to elaborate on that comment and explain why I believe (1) people are increasingly opting out of insurance coverage, (2) what insurance companies of the future will need to look like to stay alive, and (3) how adjacent consumer industries such as CPG, fitness, mobile apps, alcohol/spirits, and others will follow-suit to cater to an increasingly health-conscious population.

So, without further ado…

Prediction 1

In 1–3 years, traditional insurance coverage will no longer be considered necessary for preventative care as new, low-cost solutions emerge across digital health verticals.

Although “insurtech” has been a hot topic for a few years now, the insurance category that has evolved the least is unfortunately the one that impacts us most — health insurance. One of the first realizations I had about the severity of the broken health insurance ecosystem occurred when I was speaking to Nedal Shami, co-founder and CEO of dntl bar, a modern dentistry chain seeking venture funding.

Shami, who is also former co-founder, COO, & CGO of CityMD, mentioned that about 50 percent of dntl bar’s patients opt to pay for services out of pocket despite the business accepting almost every major insurance provider. While this may seem strange to some, opting out of insurance coverage becomes a lot more understandable when you consider that 1 in 4 millennials (25%) do not have dental insurance. Further, those who do have dental insurance may have such high deductibles that it simply doesn’t make sense to continue paying for it if low-cost alternatives exist (even if that means paying out of pocket).

Given these observations, dntl bar recently launched a $39/month self-pay membership model that covers all preventive care, including x-rays, as well as annual benefits and discounts on other services and procedures. This membership not only encourages retention, but also enables patients to get the care they need in a timely manner without paying an arm and a leg to receive it. Add to this model dntl bar’s modern and efficient online booking experience, beautiful and welcoming office spaces, and care-driven vs. diagnosis-driven practitioners, and you can begin to see the foundation of a best-in-class 88 NPS (Net Promoter Score) consumer business that is changing the way people view and experience dentistry forever, compared to the dental industry’s average NPS of 1. Tend is a formidable competitor to dntl bar that is also gaining incredible traction for similar reasons.

If you’re thinking that dentistry may be a fringe example of an industry more susceptible to this self-pay phenomenon, think again. New-age mental health companies such as Real, Coa, Pace, Bloom, Noom Mood and others are also beginning to offer modern psychology services and pathway-focused content through self-pay monthly subscriptions. Coa goes so far as to compare itself to “a gym for your mental health,” further pushing the member vs. patient ethos. Yet another segment, medical-grade dermatology businesses such as Dear Brightly and Nurx are modernizing the way patients get prescribed retinoids, birth control, and topical creams for anti-aging, acne and rosacea — all while embodying the same simple and affordable out-of-pocket, member-based business model. Moving to generalized care, providers like K Health, Sesame, Well, and Lemonaid Health (not to be confused with the equally disruptive and consumer-friendly home/renter, pet and car insurance company, Lemonade), are also following suit with the same approach.

Drawing on these examples, it’s important to note that a key underpinning behind the movement of paying out of pocket for preventative care is the consumer trend of understanding and quantifying the augmented self. The desire to leverage one’s data in exchange for more personalized services has brought about the creation of new companies aiming to re-engineer preventative care models in ways that enable higher margins and offer better services for patients across categories. Today, nearly 1 in 4 US adults report using some form of wearable device or activity tracker (approximately twice that of 2015), and 82 percent report willingness to share wearable data with their providers. Forward Health is an example of a company taking advantage of this trend to pioneer the move toward data-driven preventative care. The business combines world-class doctors with biometric health monitoring, genetic analysis, and more to offer members a modern, personalized care experience for $149/month.

All to say, the trend of opting out of insurance coverage for routine care and regular prescriptions is catching growth waves, and it’s important to recognize that this phenomenon isn’t happening because people can’t afford insurance or believe they are too healthy to opt-in. Rather, these examples serve to prove that it is becoming increasingly easy, convenient, and affordable to receive quality healthcare using modern, digital-first platforms that are equally effective as their historically complex and expensive counterparts.

Following this trendline into the future, I believe the consumerization of healthcare will continue to run its course as doctors everywhere begin experimenting with membership models that deliver higher margins for their businesses and better care for their patients, leaving insurance companies in the dust.

Prediction 2

In 5–10 years, private insurance will look a lot more like the consumer businesses we see operating around it as providers alter traditional insurance models to be more data-driven, consumer-friendly, and affordable than ever before.

While it’s true that people are increasingly opting to pay out of pocket for routine care and recurring prescriptions, it would be naive to think that insurance companies will go away for good. For one, there will always be a sickly population for which the economics of traditional insurance make sense, and two, insurance companies will inevitably innovate to maintain market share and remain whole. But what will that look like?

In 3–5 years, I predict choosing a plan that fits your needs will be more user-friendly, simple, and easy to understand. There will be no more arbitrary open enrollment deadlines, no more guessing which services are covered and which aren’t, no more jargon to explain plan details and fine print, no more surprise medical bills, no more limited in-network selection of doctors, and generally speaking, no more hassle. I know this sounds like a wild fantasy at present, but should it be? And more importantly, can it afford to be as digital health tech startups continue to eat insurance companies’ lunch?

Further looking into the future, in 5–10 years, I believe insurance companies will begin to revolutionize healthcare by paying for wellness rather than paying for sickness, as traditional insurance companies do. I recently read an article by one of the nation’s leading thinkers on health policy, John C. Goodman, called “What’s Wrong with Private Health Insurance?”. In it, Goodman explains the twisted dichotomy of the current insurance model:

“In a rational insurance world, people would pay out of pocket for inexpensive services and rely on insurance to pay for expenses that are large and rare,” he says. “The typical employer plan, however, does just the opposite.”

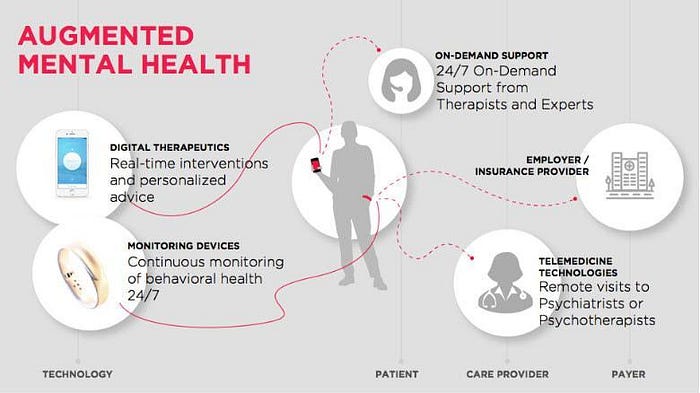

Specifically, future-forward insurance providers will look to partner with wearable brands like WHOOP, Oura, Apple, Fitbit, and others to incentivize and reward healthier lifestyles and therefore, lower patient spend and associated COGS. This looming business shift will inevitably give rise to a whole new level of data sharing, presenting the idea that people may have financial incentives to share information about their lifestyles in exchange for lower premiums. HealthIQ is an example of a company pioneering this concept for life insurance, and I predict health insurance models will follow suit, especially as people continue to adopt wearables and activity trackers as part of their personal IT suite.

The shift toward using patients’ activity scores to predict spend may also pave the way for a new category of businesses that serve as an intermediary for insurance companies to encourage healthy living behaviors among members. Vitality Group and Well Dot are two such businesses poised to pioneer this model, and I believe AI-driven health coaching apps that incorporate data from wearables to recommend actionable lifestyle changes such as Ommyx, Holly Health, and BestOfU will continue to expand their service offerings to do the same. (P.S. The latter three health coaching apps are currently raising pre-seed/seed rounds as of Dec 2021).

Some final thoughts about future plan models: (1) Gym memberships and online fitness offerings will be discounted as table stakes. (2) Fitness/activity trackers, CGMs (Continuous Glucose Monitors), and “lab-in-your hand” health diagnostics will be covered or partially covered by insurance. Companies such as Levels, Signos, Veri, Nutrisense, Vessel, Vivoo, and Lumen are already proving themselves to be effective at helping people understand their bodies to reduce stress, manage weight, optimize sleep, and more, while bio-trackers like WHOOP and Oura Ring have proved effective at detecting illnesses such as COVID prior to patients testing positive. (3) Biometric data captured through these products will begin to be used for estimation by actuaries; and (4) HIPAA and data privacy laws will need to be modified to account for such use cases. Lynx.MD is an example of a company already thinking ahead on this matter (recently raised $12 million in seed funding). The business offers revolutionary healthcare data security services designed to de-risk information that will inevitably be used by insurance companies.

Prediction 3

Adjacent spaces such as CPG, fitness, fast food, and functional beverages will follow suit, as living well becomes the new normal, not just a concern for diabetics, athletes, at-risk individuals, or health-conscious gym hardos.

In 5–10 years, I imagine a world in which food packaging will include digital integrations that advertise suggested portion sizes in correspondence to shoppers’ health scores. Sugary drinks will be priced like alcohol, and low/no-alc brands such as Haus, HOP WTR, Atopia, ISH Spirits, and Seedlip will become mainstream in all bars.

New apps like Ommyx, RxDiet, OneDrop and Tidepool that suggest meals, ingredients, and portion sizes based on users’ diet and exercise routines will eventually replace basic calorie counters and V-lookup food databases like MyFitnessPal.

Adopting continuous glucose monitors (CGMs) to track blood sugar will become mainstream — a trend that is already taking shape — and consulting your phone for real-time decision-making on what to eat and when will be as common as checking the weather.

These recommendations will inevitably expand beyond an individual’s discretion and manifest in the form of advertisements on social media, online grocery, and quick convenience eComm for sponsored snacks and ingredients that correspond to users’ health goals.

OpenTable will suggest restaurants that cater to your diet preferences vs. proximity, and the American fast-food industry will begin to look a lot different. In addition to red meat alternatives already being offered at McDonald’s, Burger King, and select Dunkin’ locations, I expect fast-food chains to incorporate more health-conscious items to their menus as they continue to compete with better-for-you fast-casual dining spots like Sweetgreen, Dig Inn, Cava, and others.

The market for mental health and mindfulness will match and exceed that of gym-goers as new entrants continue to expand upon the below categories.

Enterprise use cases for connected exercise machines such as Peloton, MIRROR, Tonal, Carbon Trainer, and Hydrow will skyrocket as gym chains, hotels, and luxury apartment buildings recognize the benefits of merging at-home fitness with in-studio offerings.

More on this last point: Imagine going to the gym and logging into the equipment you’re familiar with to continue regimens you began at home. These connected exercise machines will eventually supplement personal trainers and studio classes as gym chains begin to create their own content for equipment partnerships, encourage coaches to customize their clients’ programming via connected hardware, and deploy exercise challenges that increase retention via gamification — all while bridging the gap between at-home and in-studio experiences.

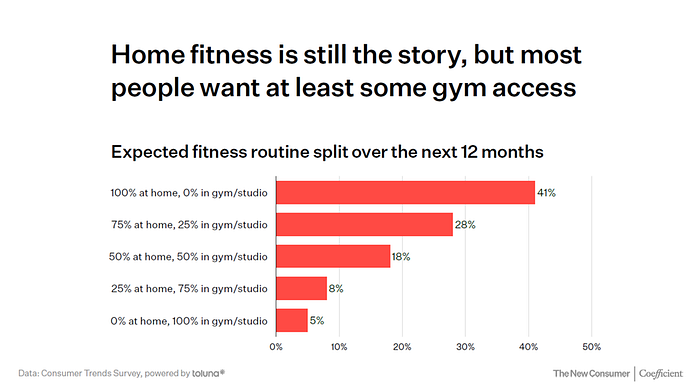

This seamless transition between at-home and in-studio will be crucial moving into 2022+ as research suggests 54% of people prefer some mix of at-home and in-studio instruction, with only 5% expecting their fitness routines to be exclusively gym-based moving forward. Expanding on this idea, famous workout studios such as Rumble, SoulCycle, and SolidCore would be wise to follow Barry’s lead in partnering with connected equipment manufacturers to feature studio-sponsored content on these devices.

TL;DR

The health and wellness industry is on the precipice of change, and although I’ve outlined a few ways in which that change may run its course in 2022+, I’m sure there’s a lot that can be hypothesized further. If you’re an entrepreneur, I hope this post gets you thinking about all the ways in which the industry has yet to be disrupted; and if you’re an investor, I hope it serves as a helpful guide for the types of businesses that may be most successful at reinventing the status quo to deliver outsized returns.

As we embark on the new year, I look forward to seeing which businesses continue to thrive, which inevitably flop, and which new entrants prove to make our lives easier, healthier, and more enjoyable.

If you’ve made it this far and want to nerd out further, please don’t hesitate to leave a comment or reach out directly: jschram22@gsb.columbia.edu. I look forward to hearing from you!